ICH ensures financial performance and market integrity through robust risk management systems.

Risk

Management

In its role as a Clearing House, Indonesia Clearing House (ICH) ensures the financial performance of every cleared trade. To maintain the integrity of the clearing system, ICH has well-established risk management systems to monitor and measure the risk exposures of its members.

The risk management framework employed ICH includes stress-testing to determine capital adequacy of the clearing fund, position limits on individual customer group to prevent excessive concentration risk, and responsive margining and collateralisation processes.

Margin &

Mark-to-Market

Margins represent assets held as collateral against the possibility of a clearing member defaulting on any financial obligation relating to its open derivative contracts.

To achieve a balance between robustness and efficiency, margin reviews are conducted on a regular basis. In addition, during adverse market conditions or whenever the situation warrants, margin reviews will be performed more frequently to ensure sufficient collateralisation of trades.

In accordance with the Futures Trading Act, each Clearing Member is required to keep customer collateral deposits segregated from its own.

Maintenance Margin

and Initial Margin

ICH maintains a two-level system (Maintenance Margin and Initial Margin) in prescribing minimum margin requirements for clearing members and customers.

Maintenance Margin represents the minimum collateral deposit that ICH requires from clearing members while Initial Margin represents the minimum collateral deposit that clearing members require from their customers for newly entered positions.

Clearing members are only obligated to collect additional margins from a customer if the margin-on-deposit falls below the level of Maintenance Margin. When this happens, a margin call is issued to the customer and margin must be brought back to the level of Initial Margin.

Margin

Methodology

ICH margining methodology has been tested extensively and proven to be adequate throughout financial crises.

Margin model seeks to cover each product’s estimated distribution of future exposure in pre-specified liquidation period at the 99% confidence level.

Historical Simulation

Single-tailed confidence level 99% based on normalized historical returns and subject to procyclicality adjustment

3 year

Weekly for major contracts;

Monthly for all contracts

Ad hoc for adverse market movement

Mark-to-Market

The primary purpose of Marking-to-Market is to prevent the accumulation of losses and limit the exposure of the Clearing House. This is achieved when the Clearing House revalues all open positions during each clearing cycle. Gains and losses for futures and OTC swaps, are collateralised together with margin requirement.

Clearing Members are expected to have sufficient funds or credit facilities to meet Mark-to-Market settlement variation calls or risk being deemed insolvent by the Clearing House.

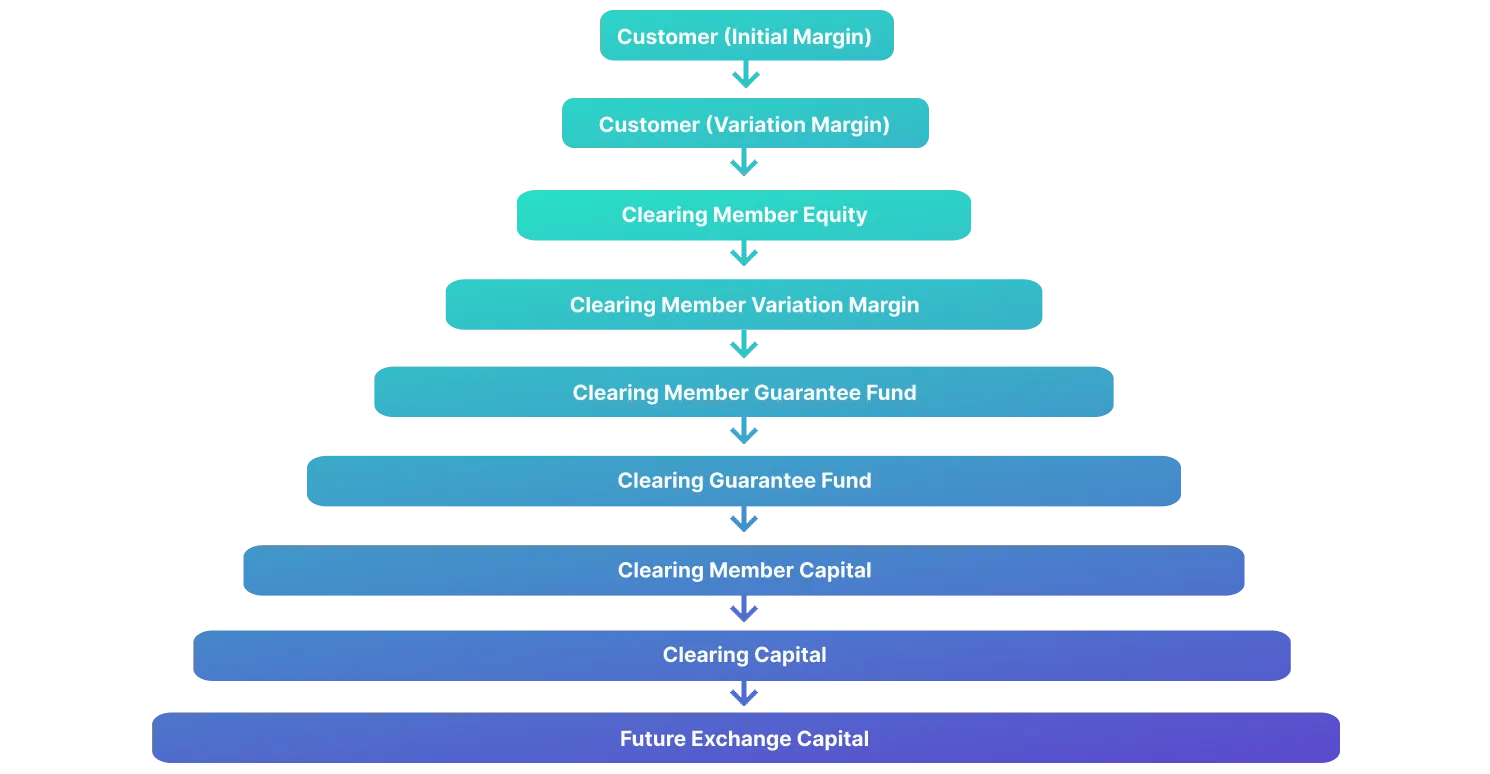

Clearing

Waterfall

The Clearing Waterfall is a layered risk management mechanism implemented by the Clearing House to manage and absorb financial losses arising from a default by a Clearing Member. This mechanism is designed to ensure that any losses are addressed in a structured, transparent, and orderly manner, while safeguarding the stability and continuity of the clearing system.

In the event of a default by a Clearing Member, the Clearing House will first utilize the financial resources provided by the defaulting Clearing Member, including margin collateral and its contribution to the Default Fund. If these resources are insufficient to cover the resulting losses, the Clearing House will subsequently activate the next layers of protection in accordance with the predetermined waterfall structure.

Indonesia Clearing House is a business entity that organizes and provides systems and / or facilities for the implementation of clearing and guarantee transactions on the Futures Exchange and is established with the aim of supporting the creation of regular, fair, efficient and effective Futures Transactions in the Futures Exchange in accordance with the mandate of law no. 32 of 1997 concerning Commodity Futures Trading and Law No. 10 of 2011 concerning Amendments to Law No. 32 of 1997.

Jl. M.H. Thamrin No.3 8th Floor, RT.11/RW.2, Gambir, Central Jakarta City, Jakarta 10110

+62 21 4050 7788